To put the issue in some sort of context, the background to this decision is undoubtedly Ben Bernanke's move in early November to extend US monetary easing, by going one bridge further in his assault on the housing deflation and continuing high unemployment which weigh down the economy by introducing what effectively amounts to a second round of exceptional policy measures (known coloquially as QE2). The leading objective behind this move was to increase the amount of liquidity available in the US economic and financial system, although a more covert consideration was cleary to weaken the dollar in an attempt to boost exports and use the strength of external demand to tow the US consumer back towards growth territory. Joining up the dots, we find that the key link between these two otherwise seemingly unrelated central bank decisions (after all one is concerned with an economy which is growing too slowly, while the other is working with one which may be growing too quickly) is to be found in the fact that the US economy is already saturated with as much liquidity as it can handle (in terms of the capacity for absorbtion of the domestic sector) and as a result the funding made available works its way through to more attractive, and more profitable outlets across the developing world.

So what has happened in practice is that large quantities of liquidity have been been seeping out of the back door, some of it undoubtedly heading over to Europe in the search for the reasonably safe but still quite attractive pickings which have become available due to the Sovereign Debt Crisis, but the lions share is surely making its way towards those, seemingly "risky" rapidly growing emerging economies.

This has lead to a certain amount of angst and confusion among developed economy political leaders, with Angela Merkel, among other European politicians, voicing the complaint that the financial markets are effectively "mispricing" risk. Personally, I don't claim to have any special insight into whether or not the markets are pricing risk well, or badly. I would have thought that that was exactly why we had markets in the first place (rather than a centrally planned pricing mechanism): to put a price on risk. But that being said, the systematic downgrading of the ageing developed world and the systematicup grading of the youthful "growth" economies in the third world has a certain logic to it.

Obviously, in a world which is as rapidly changing as ours is, markets need time to adjust. And market participants are evidently a vulnerable as anyone else is to the human failing of getting things wrong. Markets are not superhuman entities, their outcomes are the aggregated product of a very large number of individual human decisions. But I think it is important here that all concerned recognise their own limits and limitations. It is either an extremely bold or an extremely foolish politician who feels equipped to move to a higher level to pass judgement on a process whose outcome is still remains an open question. Post hoc, as we have seen in the wake of the recent financial crisis, there is no shortage of critical voices, and all and sundry have a notable facility to point the accusing finger to tell the markets "you got it wrong"! But telling them you have it wrong before the event, well that takes gall! And if you are really so sure, then put your money where your mouth is, and buy up all that debt the markets evidently don't want.

In fact, markets are neither omniscient, nor omnipotent, and often move as much behind the curve as they do in front of it, correcting to changing undelying realities in a herd-like fashion and even then only after a time lag. Yet, as I say, there is a certain logic behind the most recent trend, which involves repricing risk in the developed economies (due to their ageing populations, and large uncovered obligations with the future, issues whose importance was not sufficiently appreciated and accounted for in the pre-crisis world ), at one and the same time that risk in the developing world is also repriced, since emerging market "risk" may not be quite so risky as the "old normal" mindset used to think it was.

As a result, a number of key emerging economies find themselves in the pleasant position of enjoying the benefits of a win-win dynamic, since far from struggling with ever higher elderly dependency ratios, the proportion of their population in the labour force (and also in employment) is now rising constantly, while both inflation and interest rates (including ones related to country risk) are trending downwards in the longer run. Turkey is, in fact, one of these fortunate economies, which is why I think the latest move from the Turkish central bank needs serious consideration, and should be understood not as just one more piece of "midwinter madness", but rather seen as part of a much more calculated and comprehensive strategy which comes from a modern and continually evolving tool set. New problems need new remedies, so let's leave small open (and even large open) economies where they belong: in the unreal world of the academic textbook. In today's world interest rates are not set locally, and excessive domestic inflation is often produced more by the dynamics of global capital flows than by the irresponsible spending decisions of local politicians. Which is not to say that the Turkish central bank have the balance right (or wrong), but simply to state that global problems require global solutions, and in the meantime, national leaders will have to adapt their policy mix to confront new problems, problems which but a few short years ago would have seemed almost unimaginable.

Complex Problem Set With A Positive Outlook

As Erdem Basci, deputy governor of the central bank recently argued, strong capital inflows (see chart below), fuelled by quantitative easing in developed economies, are in danger of producing the undesireable outcome of distorting economic development in emerging economies and potentially fuelling asset bubbles in the longer run. According to Basci, as argued in a posting on the central bank website, the best policy response to this thoroughly modern problem is to try to make these countries less attractive to short-term investors by cutting interest rates in a step-by-step process (a move which would also make the country more attractive to longer term investors - think FDI), while making extensive use other tools to attack the excess liquidity problem and restrain domestic credit growth.

And so it was to be, since the central bank's monetary policy committee voted at its most recent meeting to cut the reference lending rate by 0.5% (to 6.5%). This move was rapidly followed by the second of the steps advocated by Basci, since the bank then announced that the required reserve ratios (RRRs) for Turkish banks would be lifted to 8%, a move was expected to drain an estimated 7.6 billion Turkish lira (or $4.9 billion) from the economy in one foul swoop, with the objective of reducing the amount available for Turkish banks to lend to their clients.

Now in order to make sense of this decision, the key point to grasp is that Turkey's economy is not, in fact, currently overheating. At the present time, the very opposite is happening, since the economy has been slowing, with the quarter-on-quarter growth rate falling in the third quarter to a "mere" 1.1%, down from the sweltering "China like" pace of 3.7% clocked up between April and June. Now a 1.1% quarterly GDP growth rate (or a 4.4% one annualised) is not exactly small beer by present developed economy standards, but it certainly is not overheating territory for an economy in the process of making the shift from underdeveloped to developed status in the way that Turkey's is.

Nor is inflation showing signs of getting out of hand. True, at around 7% it is still stubbornly high, but it has been stabilised, and shows no sign of getting out of hand, while the core inflation rate has been falling steady, and is now around 3%. So while the situation signals caution, it hardly cries out for drastic monetary tightening.

So what the recent decision was really about was not an attempt to conform with the objectives of conventional monetary policy, rather the move was intended to dissuade and deter speculative investments looking for higher yields from continuing to pour into Turkey and magnifying the economy’s key weakness: the mushrooming current-account deficit. The idea was to reduce the yield differential with lending rates in the quagmired developed economies.

So the problem facing Turkey's policy makers is not the economy isn't growing, or that it is growing too quickly (there is plenty of spare capacity left out there), rather the problem is that it is growing in an unbalanced way. The high yield differtial, and the funds inflow which it is producing, means that the currency is appreciating even while inflation remains excessively high (now stuff that in yourtext book and smoke it), and this combination is a sure fire way for the export sector to lose competitiveness. And this is in fact what is happening, as imports (driven by the consumer credit boom) surge, while exports fail to keep pace, with the result that the trade balance deteriorates, and along with it the current account one.

But as Erdem Basci among others, including some IMF economists, argue, hiking interest rates could be totally counterproductive in the current climate since it might well serve to make the country even more attractive (by increasing that key yield differential) to precisely the kind of funds they want to deter. Turkey, as many analysts constantly point out, has become over-dependent on the wrong kind of funding to finance its current account deficit. What Turkey needs is to attract longer term investment finance, and while reducing the volume of short term speculative finance which is currently distorting prices in the country's equity markets. This argues for lower, not higher, interest rates, since bringing the longer run cost of borrowing down should make the country more attractive to the kind of investor it needs.

So the bank have decided to adopt a monetary experiment based on a resort to other measures, and the first of these is an attempt to withdraw some liquidity from the banking system. One of the principal worries is that the rapid expansion in the volume of domestic credit has triggered a rise in imports and thus aggravated the deterioration in the current account deficit. But the problem is not only a current account deficit one. The following chart (prepared by staff at the Turkish economicresearch institute TEPAV) shows that the credit expansion is also associated with a rise in the systematic risks of the banking sector, since much of the lending is evidently being financed by short term fund flows.

[Please Click on Image to View More Clearly]

Net foreign financing of Turkey's banking sector hit US$17 billion in the last quarter of 2008. Subsequently the level fell rapidly, but with the economic recovery foreign funding has once more been on the increase, an as of October 2010 it was in the region of US$22.5 billion. One important characteristic of the foreign funding the Turkish banks have been accessing since the advent of the recovery is that something like 98 percent of the funds are short term. This sharp rise in short term funding is not only unprecedented, it is also highly dangerous, since were there to be a sudden change in risk sentiment (due to factors which had nothing directly to do with Turkey itself), such funding might not be renewed, leading to a maturity mismatch between the banks' borrowing and lending which could severely strain the Turkish financial system.

The central bank is therefore pretty concerned to slow the rate of credit expansion, and with this in mind it has also introduced a second bloc of measures involving steps to contain the rate of expansion in consumer credit - credit card restrictions, increased loan to value ratios in house purchase, etc. Due to the endless ability of those who are smart enough to find ways to get round such rules, none of these are perfect, but they are a lot better than nothing, and nothing, some will remember, was those responsible for managing the Spanish and Irish economies did when their credit and indebtedness ratios were obviously on the verge of getting out of control, and when the relevant central bank seemed to see no inconvenience at all in applying negative interest rates to their already credit-bloated economies. So by all means criticise the Turkish central bank, but let's be clear what (and who) we are comparing them with.

Obviously additional measures could and should now come from the Turkish government. Measures which involve the judicious (and even aggressive) use of fiscal policy to drain in the most direct fashion excess demand from the system. In this context it is pleasing to be able to note (see below) that this year's strong rise in tax revenues is not being matched by an equivalent increase in spending. Indeed the country is now running a quite strong primary budget surplus. More of the same, and then some, is what we need to see, but with elections looming it is doubtful decisive steps will be taken until the new government is formed.

And it isn't only rapidly growing credit that is a concern, a lot of the money has gone into Turkish stocks which are now not far off their 2008 pre-crisis highs. In fact foreign purchases of Turkish financial assets rose to around $15.5 billion in the first 10 months, from $730 million a year earlier, according to central bank data. In October alone, international investors bought $969 million in shares and $1.5 billion in government bonds.

Summing up, it is hard to say at this point whether the Turkish central banks attempt to operate what some have called a "post modern" monetary policy will work exactly as intended, especially since the outcome is not directly in the hands of the central bank, and very much depends on the determination of the government to take the necessary measures on the fiscal side. But whatever the outcome, of one thing we can be sure: doing something always has to better than doing nothing. After all, who else would knowingly and willingly wish to end up in the kind of unfortunate situation Spain and Ireland now find themselves in?

The Economy Has Surpassed Pre-Crisis Levels, And Is Now In Full Recovery Mode

Turkey's economy slowed in the third quarter, and the pace of GDP growth slipped back to a calendar adjusted 6.4% year on year in the third quarter, down from the China like 10.2% pace registered in the second one. The key to the slowdown was the deterioration in external trade: exports dropped by 2% year on year, the sharpest contraction since the third quarter of 2009, while import growth remained in double-digits for a fourth consecutive quarter (albeit slowing marginally to an annual increase of 16.9% from 18.8% in the second quarter).

Final domestic demand growth, on the other hand, strengthened to 11.2%, its fastest pace of advance in more than four years. Private consumption growth was strong, and surged by 7.6%, but the heavy lifting seems to have been done by investment (much of it in construction), with an increase in gross fixed capital formation of 31.3%. Even if the underlying housing boom offers the explanation for much of this growth, capital goods investment was also strong, as shown by the fact that the import of capital goods rose by an annual 31.3%.

In fact, the most worrying part of the Q3 performance was not the fall in exports, it was the surge in imports, and the impact this is having on the trade and current account balances. Correcting this disturbing trend must now be one of the most important policy priorities for Turkish decision makers. Consensus forecasts now suggest Turkey could well grow by an annual 7% this year (up from an earlier expectation of 6%) and this does not seem to be at all unreasonable,

Whatever the weaknesses, the big picture story is that Turkey’s economy is once more growing dynamically and reaching new highs. Real economic gains are being made and we now are seeing increasing evidence of a true recovery which goes well beyond the confines of a simple statistical rebound.

But a dose of realism is called for. Despite the fact that the economy will in all probability now grow by at least 7% in 2010, in 2011 Turkish growth rates will undoubtedly continue to drop back from the very high level seen in the first half of this year, but if this weakening in headline GDP numbers is simply the result of a deteriorating net trade position then we will have the worst of both worlds, as debt driven consumption growth will be faster than desireable, while the export sector will continue to weaken, even as import substitution undermines the domestic industrial sector. Unchecked this could lead to the same sort of manfuacturing industry job loss we have seen across Southern Europe over the last two decades.

On the other hand, the Turkish economy is likely to continue turning in an impressive performance, one which will stand out among regional peers since sustainable trend growth in Turkey remains high. If adequate steps aretaken to rein-in the current account deficit, and to attract more in the way of job-creating FDI, 6% growth could well remain a realistic target for 2011, even if there is a deterioration in the external environment and a weakening in the level of external demand.

One factor which makes Turkey stand out from many of its regional peers is that it is not overly export-dependent and has a dynamic domestic economy which complements the export sector. This means that the Turkish economy basically stands upright, and on both feet, and that, despite the recent loss of export competitiveness the impetus behind GDP growth is much more broadly-based than in the other, heavily-indebted countries which can be found in the surrounding region. In addition, the underlying strength of domestic demand means the Turkish government has a far broader, and ever-growing, potential tax base. This makes it much easier to attain longer term fiscal stability, and means that the country does not have to continually stagger forward on the basis of a series of “one off” measures to keep the deficit undercontrol.

To some extent the slackening in Turkey's growth performance is only to be expected, since, in terms of external demand (and as in many other economies) all the "low lying" fruit has now been picked as exports have steadily attained their previous level. Reaching out for the rest will now become more and more difficult, especially with so much "deleveraging" going on in the neighbourhood, and so many export dependent economies in the region, which is why the export competitiveness issue needs to be so strongly stressed.

Thus, while Turkey turned in an 11.7% annual growth rate in the first three months of the year, and then followed up with an impressive 10.3% in the second three – a rate only equalled by China among the major economies – the calendar adjusted 6.4% rate registered between July and March is better read as a return to normality rather than the commencement of a serious slowdown. Quarter on quarter the economy grew by a seasonally adjusted 1.1%, and output was still up by 8.2% in the first nine months of the year over the equivalent period in 2009.

On top of this, the economy is now reaping the long run fruits of major macro economic restructuring in the early years of this century, while in addition the country faces a very favourable demographic evolution. The result of this very fortunate combination is that the dollar denominated value of Turkish GDP is now very substantially above where it was ten years ago, and now that the recession is behind us it should continue to rise rapidly.

Current Account Woes

Throughout this year the negative balance on Turkey’s current account has steadily worsened, and the trailing 12 month deficit total in October was around $40 billion, or 5% of GDP. This underlying deterioration in parts reflects the country’s energy dependence and the impact of rising fuel costs, but it also gives a measure of the strength of the domestic consumer rebound coupled with the impact of the inflation-driven real exchange rate appreciation.

Turkey has had a long history of persistent current account deficits, and as might have been expected while the problem eased during the recession, the arrival of the recovery slammed issue straight back onto the table. During last year’s sharp contraction, Turkey’s current account deficit fell back to 2.3% of GDP, and the topic moved quietly off everyone's radar. But last year's reduction was due to very exceptional circumstances (the sharp contraction in domestic demand during the global financial crisis), so this years widening of the deficit to a level which could eventually be as high as 6% of GDP (or even slightly over) is essentially a reversion back to type. Which does not make it any the less problematic.

When thinking about competitiveness, as well as simple exchange rate movements it is also important to take inflation differential's into account. Indeed the Turkish currency has been weakening recently on the back of the European Sovereign Debt Crisis, and the lira fell to a five-month low against the dollar following the central bank announcement of the latest measures. But even prior to the rate reduction the lira had been falling, and is now down around 7.5% against the US dollar since November 4 as concern has grown about potential economic spillovers to Europe's trading partners from the growing problems in countries like Ireland, Spain and Portugal. Weakening European demand is not good news for Turkey, since Europe is Turkey's main trading partner.

Thus while the lira rose by something like 9% against the euro last year the net 2010 gain against the dollar (before the post-November 4 slide) was only about 4 percent. However, given the much closer trade ties that Turkey has with the EU, it was the Euro rate which mattered for the export performance.

Although Turkey's exports were up sharply in October (to $11 million), after several months stuck around the $9 million mark, the improved performance was not sustained, and in November they fell back again to around $9.4 billion.

But of course, in the complete picture we would have to note that imports (and with them the trade deficit) have also continued to rise steadily, although at $17.1 billion in November, they were still some considerable way below the July 2008 high of $20.5 billion.

The seasonally adjusted trade deficit has continued to deteriorate steadily since the recovery started in late 2009.

Domestic Activity Also Rises

The recent recovery in manufacturing activity continued at full pace in October, with industrial output posting an annual increase of 9.8%, well above the 6.1% market consensus expectation. Following a tame performance in September, where seasonally adjusted output stayed flat at the August level, production surged again in October, and by an eye-catching 3.1% on the month. It is worth noting that industrial production has now returned to pre-crisis levels, implying that (even though overheating is not an issue at this point) the output gap may be narrowing faster than central bank projections anticipate.

The better-than-expected increase is largely due to a strong performance in both capital and consumer-durable goods. Capital goods were up by an annual 25.6%, and consumer durables by 21.7%. While the numbers for consumer durables reflect the expansion in consumer credit, the ongoing strong performance in capital goods suggests that the investment activity also continues apace.

And the continuing strong performance registered in December's manufacturing PMI suggests the short term outlook for the Turkish industrial sector remains positive.

Commenting on the Turkey Manufacturing PMI survey, Dr. Murat Ulgen, Chief Economist for Turkey at HSBC said:

““The Turkish manufacturing sector maintained November’s impressive performance in December, expanding at its fastest rate since May. The pace of output and new order growth moderated slightly from the previous month, though still remained impressive. New export orders, on the other hand, showed the fastest improvement since October 2009. More encouragingly, this bright picture supported employment creation with conditions reaching their best level ever in the survey history. Backlogs of work increased marginally in December, while manufacturers continued to slash their finished goods inventories to meet order demand. In the meantime, this stellar performance also led to some price and margin pressures. Input prices soared at a very high rate, reminiscent of 2008 Q1 with rampant global commodity prices, whilst suppliers’ delivery times lengthened at a close to record rate. As such, manufacturers continued to reflect this in output prices that rose at the fastest pace in eight months.””

Surprisingly, while retail sales continue to grow steadily, up to now they have not been one of the leading drivers of the current expansion, as indicated by the fact that the third quarter increase was only 7.5% over a year earlier. Not bad by developed economy standards, but well short of the level of construction investment increase, for example.

Unemployment Falls Even As The Labour Force Grows and Grows

Unemployment Falls Even As The Labour Force Grows and GrowsStill, the outlook on domestic sales continues to improve, and one of the principal reasons for this is the continuing fall in the seasonally adjusted unemployment rate, which was down to 11.8% in September. In fact unemployment peaked (on a seasonally adjusted basis) at 14.8% in April 2009, and has since been falling steadily, while the seasonally adjusted level of employment continues to rise. Such strongly positive co-movements in employment and unemployment evidently lead households to have an increased sense of job security and purchasing capacity.

The country has been creating and continues to create jobs in large numbers. When compared with September 2009 the number of those employed rose by nearly a million (to around 23 million), with the share of those occupied in the industrial sector (around 20%) rising significantly.

Under the impact of the global financial crisis, Turkey’s unemployment hit a record high of 16.1% in February 2009. A year and a half later, and in sharp contrast with most of its regional peers, the country has achieved an impressive drop in its jobless rate. Even more significantly, Turkey has achieved this improvement at a time when the size of the labour force has been rising sharply, from 51.3 million to 52.7 million. This is yet another example of how Turkey is in a very different position to its regional peers, most of whom face ageing and declining labour forces due to their negative demographic trends.

In its bid to achieve ultra-fast "catch-up" economic and employment growth without generating excessively high inflation Turkey is able to benefit from the phenomenon known as the “demographic dividend.” Cutting aside the rigmarole, what this idea basically implies is that as fertility falls ever higher proportions of the population are to be found in the working age category, initially boosting employment and output, and then, in a second wave, fuelling productivity, credit and consumption growth. This is what sets the Turkish case apart, for example, from the recent experiences in places like the Baltics and Bulgaria.

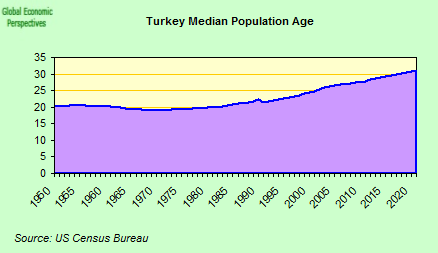

As the country's median age rises, Turkey is rapidly approaching that demographic “sweet spot” where sustainable rapid catch-up growth is totally realistic and achievable. However, it is important to bear in mind that this process is far from automatic, and depends for its effectiveness on continuing and deep structural reforms. The Turkish economy still fails to make satisfactory use of its existing labour resources, and the country’s employment rate, at just above 40%, remains the lowest in the OECD area. Deep-rooted socio-cultural factors, combined with the steady drift from rural to urban areas, mean that many Turkish women continue to withdraw from the labour force on marriage, which leaves the employment rate for women stuck around the 20% level, 40 percentage points lower than the equivalent rate for men.

Turkey's population has been growing rapidly, and will continue to grow quite rapidly for at least the next two decades. This will mean there will be an internal market with a strong growth dynamic, and that the country faces a more stable population pyramid in terms of pension and health care systems, and sovereign debt sustainability. This outlook also implies improving credit ratings and lower risk evaluation on the part of investors, with consequently lower interest rates for investment projects.

As I say, Turkey's median age is also rising, although the country is still very young, with a median age of just 28.5 and 30 per cent of the 74 million population under 18. The demographic "sweet spot" of median ages between 30 and 40 is thus set to last for some considerable period of time.

Rising median ages, and growing proportions of the population in the working age group are a product of two distinct forces, declining fertility and rising life expectancy. Turkey's fertility has been falling steadily for the last thirty years, and is now around the critical 2.1 replacement level. The key driving force behind the change is female emancipation and rising education levels. The difficult thing for the country now will be to arrest the fertility decline and maintain the birth rate around the replacement level. Unfortunately, absent a serious and sustained change in the policy approach it is far more likely that Turkey will follow the pattern already seen in Southern and Eastern Europe, and head towards very low (and therefore unsustainable in the long run) fertility levels.

Rapid Growth With Low Inflation?

Given the controversial nature of the new monetary policy experiment, it is highly the country's inflation rate will come under increasing scrutiny. After keeping its benchmark interest rate unchanged at 7% since November 2009, the central bank has now lowered the rate to 6.5%, even as the economy continues to show signs of strong growth in credit driven consumer demand.

The bank have justified their decision by highlighting the fact that core inflation rate is falling, and in fact came in under their year-end target for the first time since the central bank introduced an inflation targeting regime. They also strongly draw attention to the potential negative consequences of raising rates in an environment where this may only accelerate the inflow of short-term, speculative funding. Given that one of the key objectives of the central bank has to be reducing the level of interest rates in order to make it easier and more attractive to invest, the bank is likely to show great reluctance in moving towards monetary tightening and will most probably continue to rely on other tools to keep inflation in check, such as increasing reserve requirements to control credit growth.

Since the start of the crisis the central bank have lowered rates 14 times from their October 2008 high of 16.75%. The Bank’s stated objective is to bring the level of interest rates permanently down to well below their long term historic levels. Their ability to do this, however, is conditional on their success in reducing the endemically high levels of inflation which have continually plagued the economy.

Certainly Turkey’s inflation rate is now extremely low compared with levels considered typical only a decade ago, but it is still an upside outlier in comparison with regional peers, and in recent months it has been showing renewed signs of an uptick.

Despite the country’s secular disinflationary tend, inflation has remained stubbornly high in recent months, although it did fall for the third consecutive month in December, registering a 12 month low of 6.4%, and down from the 9.3% seen in September. Nevertheles this level is still way too high for comfort, and especially in the context of an appreciating currency. The December inflation drop was largely due to a fall in volatile food prices, which were down 2.7% from November. The ex-fresh-food-and-energy core reading has been falling all year, and stood at 3.18% in December.

This core inflation is one of the central bank’s preferred measures of underlying inflation, so they will have drawn some comfort from downward rend, but they will also have noted that producer prices rose by an annual 7.73% in December (as compared with 4.16% in December 2009), a detail which may not alarm them at this point, but which will certainly give them food for thought if the rate remains high as 2011 advances.

Public Indebtedness Is Not A Serious Problem

After many years of extremely high government deficit, Turkey has been remarkably prudent since the turn of the century . The country’s fiscal deficit has remained low since the implementation of the IMF programme, and this despite the recent crisis-generated increase. As a result, with low deficits, strong growth and high inflation debt to GDP has fallen steadily (don't start letting your mouth water Greece, this combination is impossible in a currency union). Driven up by the recession, the deficit hit 5.6% of GDP in 2009, and according to IMF projections it is expected to fall back again to 3.4% in 2011. Gross debt peaked at 45.5% of GDP in 2009, and is in the process of falling back steadily, although we shoudn't get too excited about this, since it is what you should expect to see in a country with such a comparatively young population: real pressure on the sovereign will only start as and when the population median age rises to current EU levels .

So there is little room for complacency. The recent decision by the Turkish government to shelve the proposed Fiscal Rule legislation (a measure which would have permenently committed the government to target a 1% fiscal deficit) has come in for a lot of criticism, most notably from the IMF. But caution is called for here, since the decision most likely reflects the government’s concern not to prematurely tie its hands in the face of what might be a quite closely contested election in 2011. So a wait and see attitude might be more appropriate before passing any kind of definitive judgement.

Certainly the data we have to date show quite a strong fiscal performance throughout 2010, with the government posted a primary budget surplus of TRY4.6 billion in November compared with a TRY1.2 billion deficit in the same period of 2009. Central government revenues rose by an impressive 42.4% YoY in November, while expenditures rose by 22.9%. In fact November’s results bring the year-to-date general budget deficit to TRY23.5bn – almost half of the budget deficit in January-November 2009 – and the primary surplus to TRY 23bn (Jan-Nov 2009: TRY 5.8bn), which means last years budget deficit may well come in at under the EU limit of 3%, and will in any event be significantly below the government target of 4% So despite credibility slippage, in the short term the strong economic expansion may well assuage concerns about longer term sustainability. What really matters is what happens this year, and in the years which follow. The government has budgeted for a 2.8% fiscal deficit in 2011, and given the credibility issues involved I wouldn't be surprised to see them keep to this, despite the coming election.

However, in taking what seems to be the easier path now and postponing the watertight commitment to fiscal stability for some moment in the future, the government may be storing up trouble for itself or its successor. Spending excess tax revenues is only stimulating an economy which is not in need of stimulation, whereas saving them would not only be building a cushion for the future, it would also help reduce pressure on the current account deficit by draining some demand from the economy.

Private Sector Debt Not A Problem At This Point Either

Nor is the level of private sector debt a problem, since even though it has been rising rapidly of late, the level (at around 35% of GDP) is still quite low, and relatively sustainable for a rapidly developing country.

Household debt which has been rising at rates close to 40% this year should be brought under greater control, since while current levels are not worrysome, letting these growth rates continue is not desireable.

The same goes for housing loans. The current boom in construction activity and household mortgage lending is fine, but it does need to be kept in check.

Outlook: Steady Growth, Falling Long Term Interest Rates and A Round Of Credit Rating Upgrades

So 2011 looks like it will be a pretty good year for Turkey. Of course, not everyone is convinced by the new monetary policy initiative, and the IMF have been quick to warn of the dangers. In particular they warn about the continuing practice of unsterilsed purchasing of foreign currencies. The answer here is not too difficult: sterilise, that is withdraw liquidity to compensate, which is what the bank seems intent on doing via the increase reuqired reserves.

However the IMF also warned of the danger that, even if sterilised, large purchases by the central bank could become unsustainable, given the aggressive nature of the liquidity withdrawals which would be required to maintain the stance. Undeterred by the davice, on 21st December 21st Bank Governor Durmus Yilmaz announced that the Bank was not only set on continuing its policy of carrying out forex purchases, it was actually going to increase them, taking the amount of its daily foreign-exchange purchases (as of January 3rd 2011) from US$40m to US$50m. It is quite possible the IMF have a serious point here, and the bank may do well to consider more actively their proposal that the Bank apply the increased reserve requirements on both TRY and forex denominated accounts, and that they also extend coverage of the requirements to other credit providers and instruments in an attempt to rebalance the maturity profile of their borrowing, ie reduce their dependence on short term borrowing.

On the other hand, while one EU sovereign after another finds itself facing ever increasing borrowing costs, the process in Turkey moving in the opposite direction. Just last week Turkish bond yields extended a record low, registering their steepest two-day decline in almost eight months on speculation inflation will continue to slow, thus allowing the central bank to cut its interest rates even further. The Turkish lira depreciated to its weakest levl in six months last week, touching 1.5683 per dollar at one point last Friday. The yield on the benchmark two-year lira bond closed the week at 6.98 percent after the two-year debt yield fell below 7 percent for the first time ever on Wednesday.

So far, then the policy is working, even if it is early days yet. Lower bond yields may also be favoured by forthcoming credit upgrades. Fitch Executive Edward Parker stated last month that while the Central Bank faced many challenges in 2011, Turkey’s sovereign credit rating would be positively affected if the new policy proves successful. Fitch currently has a local and foreign-currency bond rating for Turkey of BB+, one level below investment grade.

He also noted that Turkey’s sovereign rating would be positively affected if Turkey’s debt to GDP ratio continued to decline and if there were no change in political stability following the general elections. In effect it is not likely that Turkey will become an investment grade country until after the June general elections since the rating agencies will want to see the results of the revised monetary policy stance, the fiscal performance ahead of the general elections and the political landscape following them before making this kind of rating upgrade. That being said, it is perfectly possible that both Moody’s and S&P's (which currently rate Turkey at Ba2 and BB, respectively, that is more than one notch below investment grade) could make an initial upgrade in Turkey’s sovereign rating (by one notch say) even before the general elections are held.

The outlook for Turkey is thus extremely positive, even if there are concerns about the short term bias in bank funding, and longer term worries about structural distortions from the current account deficit. On the fiscal side the government is likely to have reduced the budget deficit to below 4% of gross domestic product in 2009 from 5.5% in 2009, and is quite likely to fulfil its targe of 2.8% this year, making it one of the very few countries in the EU orbit to come in with a deficit within the 3% official target level. So while there are no guarantees that the latest initiative from the Central Bank will work, there are grounds for hope and expectation that both they and the government will make changes and search for solutions even if they don't.

No comments:

Post a Comment